by Farley Webmaster | Oct 10, 2017

INTRODUCTION

Turn on the television or scroll through Facebook, and chances are you’ll see at least one advertisement for a group or “guru” who promises to teach you how to “get rich quick” through real estate investing. The truth is, much of what they’re selling are high-risk tactics that aren’t a good fit for the average investor. However, there is a way to make steady, predictable, low-risk income through real estate investing. In this blog post, we’ll examine the tried-and-true tactics that can be used to increase your income, pay off debt … even fund your retirement!

WHY INVEST IN REAL ESTATE?

One of the basic principles of real estate investment lies in this fact: everyone needs a place to live. And according to the Bureau of Labor Statistics’ most recent Consumer Expenditures Survey, housing is typically an American’s largest expense.1

But there are other reasons why real estate is a great investment choice, and we’ve outlined the top five below:

1. Appreciation

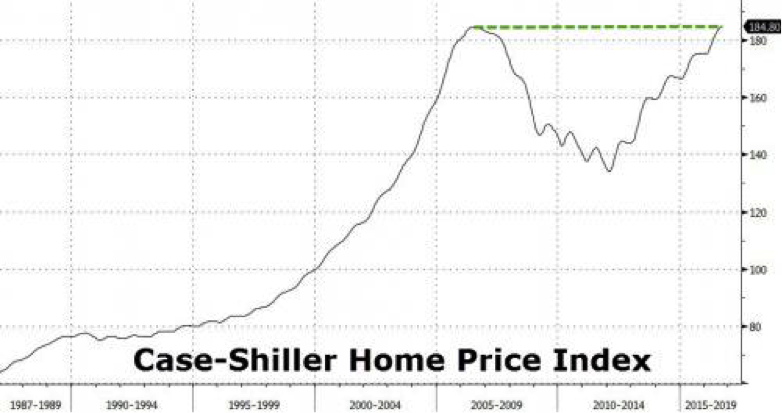

Appreciation is the increase in your property’s value over time. History has proven that over an extended period of time, the value of real estate continues to rise. That doesn’t mean recessions won’t occur. The real estate market is cyclical, and market ups and downs are natural. In fact, the U.S. housing market took a sharp downturn in 2008, and many properties took several years to recover their value. However, in the vast majority of markets, the value of real estate does grow over the long term.

The S&P CoreLogic Case-Shiller National Home Price Index, which tracks U.S. residential real estate prices, released its latest results on August 29 with the headline “National Home Price Index Rises Again to All Time High.”2

Source: ZeroHedge3

While no investment is without risk, real estate has proven again and again to be a solid choice to invest your money over the long term.

2. Hedge Against Inflation

Inflation is the rate at which the general cost of goods and services rises. As inflation rises, prices go up. This means the money you have in your bank account is essentially worth less because your purchasing power has decreased.

Luckily, real estate prices also rise when inflation increases. That means any money you have invested in real estate will rise with (or often exceed) the rate of inflation. Therefore, real estate is a smart place to put your money to guard against inflation.

3. Cash Flow

One of the big benefits of investing in real estate over the stock market is its ability to provide a fairly steady and predictable monthly cash flow. That is, if you choose to rent out your investment property to a tenant, you can expect to receive a rent payment each month.

If you’ve invested wisely, the rent payment should cover the debt obligation you may have on the property (i.e. mortgage), as well as any repairs and maintenance that are needed. Ideally, the monthly rental income would be great enough to leave you a little extra cash each month, as well. You could use that extra money to pay off the mortgage faster, cover your own household expenses, or save for another investment property.

Even if you only take in enough rent to cover your expenses, a rental property purchase will pay for itself over time. As you pay down the mortgage every month with your rental income, your equity will continue to increase, until you own the property free and clear … leaving you with residual cash flow for years to come.

As the owner, you will also benefit from the property’s appreciation when it comes time to sell. This can be a great way to save for retirement or even fund a child’s college education. Purchase a property when the child is young, and with a little discipline, it can be paid off by the time they are ready to go to college. You can sell it for a lump sum, or use the monthly income to pay their tuition and expenses.

4. Leverage

One of the unique features that sets real estate apart from other asset classes is the ability to leverage your investment. Leverage is the use of borrowed capital to increase the potential return of an investment.

For example, if you purchase an investment property for $100,000, you might put 10% down ($10,000) and borrow the remaining $90,000 in the form of a mortgage.

Even though you’ve only invested $10,000 at this point, you have the ability to earn a profit on the entire $100,000 investment. So, if the property appreciates to $120,000 – a 20% increase over the purchase price – you still only have to pay the bank back the original $90,000 (plus interest) … and you get to keep the $20,000 profit.

That means you made $20,000 off of a $10,000 investment, essentially doubling your money, even though the market only went up by 20%! That’s the power of leverage.

5. Tax Advantages

One of the top reasons to invest in real estate is the tax benefit. There are numerous ways a real estate investment can save you money each year on taxes:

Depreciation

When you record your income from a rental property on your annual tax return, you get to deduct any expenses associated with the investment. This includes interest paid on the mortgage, maintenance, repairs and improvements, but it also includes something called depreciation.

Depreciation is the theoretical loss your property suffers each year due to aging. While it’s true that as a home ages it will structurally need repairs and systems will eventually need to be replaced, we’ve also learned in this post that the value of real estate appreciates over time. So getting to claim a “loss” on your investment that is actually gaining in value makes real estate an appealing investment choice.

Serial Home Selling

Even if you’re not interested in owning a rental property, other types of real estate investments offer tax advantages, as well. Generally, when you own an investment property you pay a capital gains tax on any profits you make when you sell the property.

However, when you sell your principal residence, you are exempt from paying taxes on capital gains (up to $250,000 for singles and $500,000 for couples). The Internal Revenue Service (IRS) only requires that you live in the house for two of the previous five years. That means you can purchase an investment property, live in it while you remodel it, and then sell it for a tax-free profit two years later. This can be a great way to get started in real estate investing.

Section 1031 Exchanges

In addition to profiting off of your personal residence tax free, it is possible to sell an investment property tax free if you do it through a 1031 Exchange. If structured properly, the IRS Tax Code enables an investor to sell a property and reinvest the proceeds in a new property while deferring all capital gains taxes.

Tax-Deferred Retirement Account

It’s a common misconception that you can only purchase financial instruments (i.e. stocks, bonds, mutual funds, etc.) through an Individual Retirement Account (IRA) or 401(k). In actuality, the IRS allows individuals to invest retirement funds in real estate and other alternative types of investments, as well. By purchasing your investment property through an IRA, you can take advantage of all of the tax savings these accounts offer.

Be sure to consult a tax professional regarding all tax matters related to your real estate investments. If structured correctly, the profits you earn on your real estate investments can be largely shielded from tax liability. Just another reason to choose real estate as your preferred investment vehicle.

TYPES OF REAL ESTATE INVESTMENTS

While there are numerous ways to invest in real estate, we’re going to focus on three primary ways average investors earn money through real estate. We touched on several of these already in the previous section.

1. Remodel and Resell

HGTV has countless “reality” shows featuring property flippers who make this investment strategy look easy. Commonly referred to as a “Fix and Flip,” investors purchase a property with the intention of remodeling it in a short period of time, with the hope of selling it quickly for a profit.

This is a higher-risk tactic, and one for which many of the real estate “gurus” we talked about earlier claim to have the magic formula. They promise huge profits in a short amount of time. But investors need to understand the risks involved, and be prepared financially to cover additional expenses that may arise.

Luckily, an experienced real estate agent can help you identify properties that may be good candidates for this type of investment strategy… and help you avoid some of the pitfalls that could derail your plans.

2. Traditional Rental

One of the more conservative choices for investing in real estate is to purchase a rental property. The appeal of a rental property is that you can generate cash flow to cover the expenses, while taking advantage of the property’s long-term appreciation in value, and the tax benefits of investing in real estate. It’s a win-win, and a great way for first-time investors to get started.

And according to the U.S. Bureau of Labor Statistics, rents for primary residences have increased 21.9 percent between 2007 and 2015 as demand for rental units continues to grow.1

3. Short-term Rental

With the huge movement toward a “sharing economy,” platforms that facilitate short-term rentals, like Airbnb and HomeAway, are booming. Their popularity has spurred a growing trend toward dual-purpose vacation homes, which owners use themselves part of the year, and rent out the remainder of the time. There are also a growing number of investors purchasing single-family homes for the sole purpose of leasing them on these sites.

Short-term rentals offer several benefits over traditional rentals, which many investors find attractive, including flexibility and higher profit margins. However, the most profitable properties are strategically located near popular tourist destinations. You’ll need an experienced real estate professional to help you identify the right property if you want to be successful in this highly-competitive market.

DOES REAL ESTATE INVESTING SOUND TOO GOOD TO BE TRUE?

We’ve all heard stories, or maybe even know someone, who struck it rich with a well-timed real estate purchase. However, just like any investment strategy, a high potential for earnings often goes hand-in-hand with an increase in risk. Still, there’s substantial evidence that a well-executed real estate investment can be one of the best choices for your money.

Purchasing a home to remodel and resell can be highly profitable, as long as you have a trusted team in place to complete the remodel quickly and within budget … and the financial means to carry the property for a few extra months if delays occur.

Or, if you buy a house for appreciation and cash flow, you can ride through the market ups and downs without stress because you know your property value is bound to increase over time, and your expenses are covered by your rental income.

In either scenario, make sure you’re working with a real estate agent who has knowledge of the investment market and can guide you through the process. While no investment is without risk, a conservative and well-planned investment in real estate can supplement your income and set you up for future financial security.

If you are considering an investment in real estate, please contact us at 303.475.6269 or john@john-farley.com to set up a free consultation. We have experience working with all types of investors and can help you determine the best strategy to meet your investment goals.

Sources:

- Bureau of Labor Statistics Consumer Expenditure Survey Annual Report – https://www.bls.gov/opub/reports/consumer-expenditures/2015/home.htm

- S&P Dow Jones Indices Press Release –

https://www.spice-indices.com/idpfiles/spice-assets/resources/public/documents/574349_cshomeprice-release-0829.pdf?force_download=true

- Durden, T. (2016 November 29). US Home Prices Rise Above July 2006 Levels, Hit New Record High [blog post] ZeroHedge –

http://www.zerohedge.com/news/2016-11-29/us-home-prices-rise-above-july-2006-levels-hit-new-record-hig

h

SaveSave

by Farley Webmaster | Sep 14, 2017

When you’re buying or selling a home, it’s crucial to work with a qualified real estate agent. Not just a professional, but an amazing agent and a market expert. So how do you ensure you’re hiring an amazing real estate agent?

There are currently more than two million real estate professionals in North America.1,2 With so many options to choose from, how does a prospective home buyer or seller choose the right agent or broker? According to the National Association of Realtors®, trust and reputation are the top deciding factors consumers use when hiring an agent.3

But how do you measure trust and reputation … and what criteria can be used to help you make your decision?

In this guide, we’ve outlined the top attributes that amazing agents possess, as well as the questions you can ask to make sure you’re working with the right market expert to achieve your real estate goals.

5 ATTRIBUTES OF AN AMAZING AGENT

Not all real estate professionals are the same. Following are five key attributes of amazing agents to help you understand what makes top agents and market experts stand apart from the competition:

1. A Pricing Specialist: For buyers, amazing agents have a strong understanding of market trends to help you identify and secure a deal to ensure you get the home you want, within your desired budget. For sellers, market experts have experience pricing homes optimally for the market, helping you sell for your desired price, and avoid costs like additional mortgage and utility payments.

Takeaway: Whether buying or selling a home, pricing can be tricky. Market experts can help navigate best-possible pricing strategies, and also secure the home you want within your budget.

2. An Effective Time Manager: The average agent may not be utilizing the latest tools and technology to make the transaction easier and more cost effective for you. Market experts have tools and strategies at their disposal to minimize the amount of time you spend on the process. For sellers, they can also ensure you only deal with qualified buyers, not “window shoppers” who waste your time. For buyers, a market expert knows how to prioritize your needs and wants to find you the ideal home within your budget, without wasting your time on houses that aren’t a fit or are likely turn up major issues in an inspection.

Takeaway: Even a well-intentioned agent may not have the skills, tools or technology to make the experience easy for you. There are lots of hidden activities that may take up unexpected time, and a market expert will save you time and energy.

3. A Market Insider: While most agents can pull market stats about a neighborhood, community or city, they may not understand important trends or developments that would affect your transaction. Market experts live and breathe local real estate and know the trigger points for buying and selling in your market. We also stay current on effective marketing and negotiation practices, resulting in our track record of success.

Takeaway: An experienced real estate agent is often the best source of information about a city, neighborhood, or even street … we’re literally conducting market research every day.

4. A Strong Negotiator: Amazing agents truly set themselves apart in their ability to negotiate. Real estate negotiations take skill, experience and a knowledge of how to fight for your client’s best interests. While any agent can enter negotiations to buy or sell a home, experienced Realtors understand what to do before entering negotiations (establishing the upper hand), as well as during the process (when to offer or accept concessions) in order to set up the best outcome.

Takeaway: Working with a market expert will help ensure you get the best deal on your terms, not just the fastest deal.

5. An Effective Closer: Closing a deal fast is often a good thing. However, top real estate professionals know how to not only achieve your real estate goals quickly, but in the right way to avoid pitfalls. Just like negotiations, the paperwork and process of closing a real estate transaction are complicated. Market experts have a strong understanding of the contracts, timelines, clauses and contingencies within the closing process.

Takeaway: Real estate transactions often involve a significant investment, so even a small mistake can mean serious trouble. With that in mind, it’s best to work with a true market expert.

5 QUESTIONS TO ASK YOUR REAL ESTATE AGENT

The first step would be to “shop around.” Many people work with the first agent they come across without a firm understanding of their level of experience. It’s always a good idea to interview a number of agents before selecting one. If you’ve gotten referrals from people you trust, then you may only need to interview 2-3 agents.

However, it can be tough to know what to ask in the interview process. Here are some questions that can help you qualify the best agent to help you achieve your real estate goals:

1. Can you send me some information about yourself? Look for professionalism and consistency. What are their accomplishments? See how they approach their work. If they’re a newer agent, ask about their team’s dynamic and accomplishments.

2. How long have you been in real estate? While longevity is important, even more telling are the number of transactions they have closed or been involved in. So feel free to also ask: “How many homes have you sold in this area?”

3. What will you do to keep me informed? Will the agent be able to meet your expectations? Determine how much communication you want, and then find an agent who will give you the attention and time you deserve.

4. Can you provide me with further resources I may need? From market reports and pricing trends to school performance and crime statistics, top agents should have resources at their disposal … or know where to find them.

5. Seller only: Can you share with me your plan to market my property? Many agents will simply put your home in the MLS and wait for it to sell. An amazing agent should have a detailed plan of how to get your home exposure on social media, to their local networks, and more.

GET STARTED

Now that you’re armed with the 5 Attributes of Amazing Agents and the Top Questions to ensure you work with the best possible real estate agent, you’re ready to start interviewing agents.

We’d love an opportunity to win your business. Schedule a free consultation with us to find out how true market experts can help you achieve your real estate goals!

Sources:

1. National Association of REALTORS –

https://www.nar.realtor/field-guides/field-guide-to-quick-real-estate-statistics

2. Financial Post –

http://business.financialpost.com/personal-finance/mortgages-real-estate/canada-housing-bubble-agents/wcm/b49d4e3a-bd8d-4d1c-9566-bd3d80c8e23a

3. National Association of REALTORS –

https://www.nar.realtor/reports/highlights-from-the-profile-of-home-buyers-and-sellers

by Farley Webmaster | Aug 30, 2017

More than 77 percent of people own a smartphone.1 The average person checks their smartphone 46 times a day, with people under the age of 24 checking it an average of 74 times a day.1 We check it while we’re waiting in line and during our leisure time, whether we’re scrolling through social media, reading emails or getting up-to-date on the latest news.

Smartphones are not only a useful tool for communication. With the following apps, you can get organized (whether you plan to buy or sell), save money, learn about the homes in your neighborhood and get inspired for your next renovation project. If you’re like 81 percent of people, you have your smartphone with you during most of your waking hours; let it help you stay organized and make your life easier.3

Apps For Homeowners: Get Renovation Inspiration

These apps not only offer ideas for your next remodel or home décor project, some of them even give you a preview of what your home may look like once it’s finished.

1.) Houzz (Free)

The Houzz app is the number one app for home design and it’s no wonder; the app gives you access to all the inspiration, blogs and design ideas from the Houzz site on your phone or tablet. The app features View in My Room 3D, which allows you to view products in your home before you buy. Just take a photo of the space and a 3D version of the product will appear. Browse products, save photos of designs you’d like to view later and connect with local professionals in your area. Whether you’re gathering ideas for your next renovation and décor project or you’re just browsing, the Houzz app will satisfy all your design needs. (Android, iOS)

2.) iHandy Carpenter ($1.99)

Make sure the photos, shelves, mirrors and other artwork you hang are even and aligned with this helpful app. It’s an all-in-one tool kit that features a plumb bob, surface level, bubble level bar, ruler and protractor. No need to purchase these tools separately; just hold your smartphone up to the wall and the app will take care of the rest. (iOS, Android)

3.) Color911 ($3.99)

If you’re thinking of changing the color scheme of your home or want to find the right shades for lamp shades, rugs or throw pillows to match your vintage sofa, the Color911 app provides pre-selected color palettes to match any color scheme. Take a photo of the room or the furniture and the app will create a custom palette full of complementary colors. Write notes about your palette and organize it all into folders to share with family, friends or your design professional. (iOS)

Bonus Apps for Homeowners:

AroundMe (Free)

Hungry and looking for a local hotspot? Meeting friends at a coffee shop nearby? Or just need to find the closest ATM? AroundMe allows you to search for the nearest restaurants, banks, gas stations, book a hotel or find a movie schedule close to where you live. Open the app and start learning more about your neighborhood. (iOS, Android, Windows)

BrightNest (Free)

From keeping things clean to making them colorful, Brightnest, developed by Angie’s List, is loaded with suggestions on how to make your home a better place to live. With categories of customized tips (money-saving, cleaning, eco-friendly, healthy, cooking, and creative) there are plenty of great ways to pull inspiration from the app. BrightNest will help you tackle important home tasks with easy-to-follow instructions, a personal schedule and helpful reminders. (iOS, Android, Web)

Apps For Sellers: List & Sell Your Home Quickly

Are you a homeowner who is thinking of selling? If you’re preparing to sell, you know there are a lot of tasks to complete before putting your home on the market. These apps help you manage your to-dos so you can list and sell your home more efficiently with fewer distractions.

4.) Homesnap (Free)

Using the Homesnap app, you can snap a photo of any home, nationwide, to learn more about it. When you’re ready to sell, snap a few of the homes in your neighborhood to find out their valuation. This app isn’t perfect, which is why you should always consult with a local real estate agent. However, it can give you a general idea of the value of your home compared to others in the neighborhood. (iOS and Android devices)

5.) Docusign (Free)

Use the DocuSign app to complete approvals and agreements in hours—not days—from anywhere and on any device. Quickly and securely access and sign any documents. The benefit to using the app (over your desktop computer) is you will receive push notifications when a document is waiting for your signature and you can view and organize all your docs on-the-go. Using the easily downloadable app, receive and sign documents for free. You can receive and sign documents for free, but will need a paid account to send documents; pricing starts at $10 a month. (iOS, Android, Windows, Web).

6.) Wunderlist (Free)

Designed for use on the Web and mobile devices, Wunderlist is a well-designed to-do list and task management program that makes it easy to create a list and add tasks, due dates and reminders. Organize your ideas or focus into separate lists or create tasks within one list. You can also email them with whomever you collaborate, such as a spouse or your real estate agent. (Android, iOS, Windows Phone, Web)

Bonus App for Sellers:

Real Estate Dictionary (Free)

Not sure what all those industry specific terms mean? Search thousands of words and phrases from real estate, mortgage, and financial dictionaries for clear, in-depth definitions. This is a handy app for anyone who’s buying or selling and wants to learn more about the process. (iOS, Android)

Apps For Renters: Get Ready to Buy

Not ready to buy a home just yet? These apps will help you get into the perfect rental while you save money, build a budget and get on track for homeownership.

7.) Mint (Free)

Do you know where your money goes each month? Manage your bills, budget and credit score all in one place. Mint is a free app that helps you view your complete financial picture and track your spending. We recommend this app to anyone, but it’s especially useful for renters who need to crack down on their spending in order to save for a down payment. Use Mint to look for areas you can cut spending in order to save a little extra each month. (iOS, Android)

8.) Acorns ($1 a month to start)

Acorns is modernizing the practice of saving loose change with their automated savings tool. The app rounds up your purchases on linked credit or debit cards, then sweeps the change into a computer-managed investment portfolio. Acorns is free for four years for college students and everyone else pays $1 a month until their account balance hits $5,000, then 0.25% of their account balance per year. This is a useful tool for those who have a hard time saving. (iOS, Android)

9.) Neighborhoods & Apartments

Built for the on-the-go apartment hunter, this app from Walk Score takes the hassle out of finding your next home or apartment and helps you live near the people and places you love. They collect listings from top rental listing sites and we like them because they share how walkable each address is, determined by access to public transit, things to do, bike trails, shorter commutes, etc. (iOS, Android)

Bonus Apps for Renters:

Wally (Free)

Wally is a personal finance app that helps you compare your income to expenses, so you can understand where your money goes each month, and set and achieve goals. Wally lets you keep track of the details as you spend money: where, when, what, why, & how much. We love how simple it is to set a personalized savings target and scan receipts. (iOS, Android)

Credit Karma (Free)

If you’re preparing to buy, boosting your credit score is likely a goal you’ve set. Credit Karma is a free app that allows you to safely monitor your score and receive updates on ways you can improve it over time. They provide financial calculators and educational articles to help you better understand what credit is all about. Check as often as you want, and it doesn’t hurt your score. (iOS, Android, Web)

Apps for Buyers: Find the Perfect Home

When you’re ready to buy, there are several apps that can help you stay on top of the process. Whether you’re browsing online at different neighborhoods and homes and can’t seem to remember where all your saved data and information went or you want to save an important task or a neighborhood or listing clipped from the Web, these apps help you keep it all straight.

10.) Dwellr (Free)

Dwellr is run by the U.S Census Bureau and provides demographic information about the neighborhoods you are considering moving to. You get a variety of education/school, real estate, transportation, and population statistics to give you an idea of what it would be like living there. If you want to get the feel of a potential neighborhood, then Dwellr may just be the app to help you find the best home. (iOS, Android)

11.) Evernote (Free for the Basic version, $34.99 per year for Plus and $69.99 per year for Premium)

Collect ideas, notes and images in one place to access later on your computer, tablet or smartphone. Categorize your notes so you can find them quickly and easily and share them with others in a group notebook. Add the Web Clipper feature to your browser and clip and save articles, blogs and images from the Web. Whether you’re collecting research on a business idea or you’re looking for inspiration for a home renovation, Evernote can help you keep it all together. (Web, iOS, Android)

12.) Mortgage Calculator (Free)

There are a lot of free mortgage calculators available for download that will help you quickly determine what your monthly payment will be while you’re house hunting. We recommend picking your favorite and using it to help you shop in your price range. These numbers should be used as a guide, work with your agent and mortgage professional to learn exactly what type of loan you’ll qualify for. (Web, iOS, Android)

Bonus App for Buyers:

Google Maps (Free)

Google Maps is a must-have for anyone who’s house hunting. When you’re ready to visit a property or check out a neighborhood, you can use Google Maps to give you turn by turn directions to the house. You can use their satellite view to get a good idea how far important things like schools, parks, shopping, bus stops, and restaurants are to a home you are interested in and check out the other houses on the street. (Web, Android, iOS,)

Ready to move beyond the app?

If you’re thinking of buying or selling your home, or know someone who is, keep us in mind because we’re happy to help!

Source: 1. Pew Research Center, January 12, 2017 http://www.pewresearch.org/fact-tank/2017/01/12/evolution-of-technology/

- Deloitte, 2016 global mobile consumer survey: US edition https://www2.deloitte.com/us/en/pages/technology-media-and-telecommunications/articles/global-mobile-consumer-survey-us-edition.html

- Gallup, July 9, 2015 http://www.gallup.com/poll/184046/smartphone-owners-check-phone-least-hourly.aspx

by Farley Webmaster | Jul 19, 2017

Understanding a home’s true market value is about more than pictures, software assessments and price-per-square-foot. Whether you’re a current homeowner thinking of selling or are house-hunting, it’s crucial you understand what factors affect home valuation. By partnering with a local market expert, sellers will avoid pricing their house out of the market (the kiss of death in real estate) and buyers will ensure they get a good deal on their next home.

So, how do you accurately calculate a home’s value? After all, the value a home is assigned by its town or county and the one it’s given when it’s listed are often dramatically different from one another. Which one is accurate and what does it all mean? Read on to learn more.

Assessed Value vs Market Value: What’s the difference?

When it comes to home value, you’ll often hear two terms, assessed value and market value.

A home’s assessed value is often the lower number of the two, and is the value given by your municipality or county. Investopedia defines assessed value as “the dollar value assigned to a property to measure applicable taxes.”1 Although property tax laws vary, assessors commonly arrive at this number by taking into account the following:

- What comparable/similar homes are selling for in your area.

- The value of recent improvements.

- Income from renting out a room or space on the property.

- How much it would cost to rebuild on the property.

A home’s market value, or Fair Market Value, is the price a buyer is willing to pay or a seller is willing to accept for a property. A skilled real estate professional will arrive at the value using a variety of metrics, including:

- External characteristics, such as lot size, home style, the condition of the home and curb appeal.

- Internal characteristics, such as the number of rooms and their size, the type and condition of the heating or HVAC system, the quality and condition of construction, the flow of the home, etc.

- The sales price of comparable homes that have sold in your area.

- Supply and demand; that is, how many buyers and sellers are in the area.

- Location; that is, the quality and desirability of your neighborhood and other community amenities.

Why are these values often so different? An assessor usually estimates your property’s market value during a reassessment or if you make a physical change or improvement to it.2 As a result, a property may not be reassessed for many years. While your home’s market value may fluctuate with the market, your home’s assessed value is more likely to remain steady.3

What Determines a Home’s Value?

You’ve likely heard the motto of real estate: “Location, location, location.” This means a home’s value relies on its location. While the home and structures on the property will likely depreciate over time, the land beneath it tends to appreciate. Why? Land is in limited supply and a growing population puts increased demand on the housing supply. As a result, values increase.4

Other factors that affect your home’s value include the function and appearance of the property, how well the home and other structures are maintained and whether the home is a lifestyle property, such as a ranch style with mountain views or beach bungalow.

Ultimately, the best indication of a home’s value is the overall supply and demand of the market. This is why we recommend you partner with a real estate professional who takes all of these factors—the assessed value, local market conditions, home features and has physically walked through and experienced your home— into consideration to determine the most accurate market value.

How to determine if a property is comparable to yours.

Both assessed value and market value are partially determined by the sales price of similar, or comparable, homes in the area. To determine if a home is comparable to yours, look for the following characteristics:

- Lot size

- Square footage

- Home style or similar architecture

- Age

- Location

While you may not find a home with the same exact characteristics as yours, you’ll likely find a few that are close. To account for any disparity, adjust the sales prices of the comparable properties. Look at the differences between your property and the one in question and determine if the differences increased or decreased the sales price and by how much. For example, if your home has two bathrooms and a similar home only has three, estimate how much that extra bathroom increased the sale price of the similar home. The adjusted sale price is the estimation of what the property would sell for if the properties were exactly the same.2

Where can you find comparable sales?

Fortunately, you can find comparable home sales in a variety of places.2

- Your local assessor’s office is able to provide a list of recent sales you can browse and compare or a sales history of a particular house, home style or neighborhood.

- Your municipality. Many cities keep local sales information in their offices or post it online.

- Online databases, such as a real estate database

- Your local newspapers may offer some real estate information in the form of quarterly sales reports in the business or real estate sections of the newspaper.

- Our office. We regularly do Comparable Market Analysis of homes in our local area.

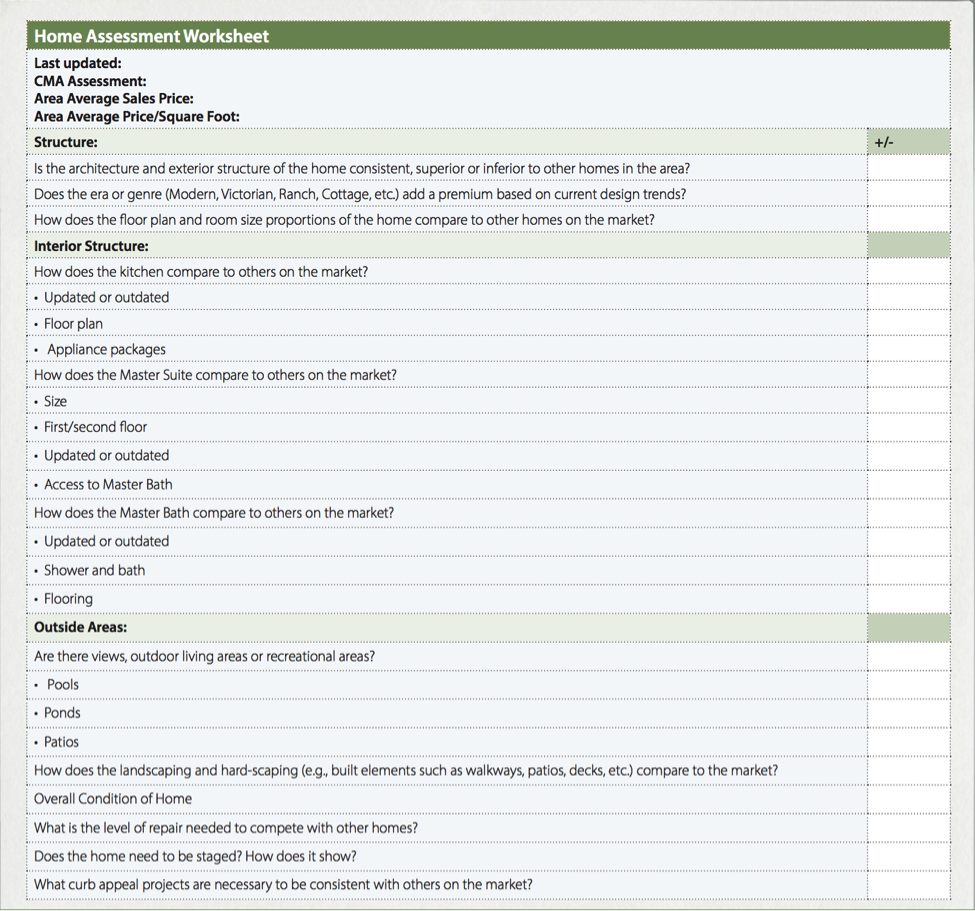

How to calculate your home’s value.

By answering a few questions about your home, property and the local market, you can begin to estimate your property’s value. We’ve also included a worksheet for you below…

Home Value Questions:

When was your home last assessed?

What was its CMA assessment value?

What is your area’s average sales price?

What is your area’s average price/square foot?

Structure:

- Is the architecture and exterior structure of the home consistent, superior or inferior to other homes in the area?

- Does the era or genre (Modern, Victorian, Ranch, Cottage, etc.) add a premium based on current design trends?

- How does the floor plan and room size proportions of the home compare to other homes on the market?

Interior Structure:

- How does the kitchen compare to others on the market?

- Updated or outdated

- Floor plan

- Appliance packages

- How does the Master Suite compare to others on the market?

- Size

- First/second floor

- Updated or outdated

- Access to Master Bath

- How does the Master Bath compare to others on the market?

- Updated or outdated

- Shower and bath

- Flooring

Outside Areas:

- Are there views, outdoor living areas or recreational areas?

- How does the landscaping and hard-scaping compare to the market? (e.g., built elements such as walkways, patios, decks, etc.)

Overall Condition of Home

- What is the level of repair needed to compete with other homes?

- Does the home need to be staged? How does it show?

- What curb appeal projects are necessary to be consistent with others on the market?

Home Assessment Worksheet

If you want to accurately assess a home’s value, it’s crucial to know about the market activity of our local area. We can help! Give us a call at 303-475-6269 to get the scoop on the local market.

Sources:

- Investopedia http://www.investopedia.com/terms/a/assessedvalue.asp

- New York State Department of Taxation and Finance https://www.tax.ny.gov/pubs_and_bulls/orpts/mv_estimates.htm

- Realtor.com http://www.realtor.com/advice/sell/assessed-value-vs-market-value-difference/

- Investopedia, http://www.investopedia.com/articles/mortgages-real-estate/08/housing-appreciation.asp?lgl=myfinance-layout

SaveSave

SaveSave

by John Farley | Oct 28, 2016

What is Home Equity?

Home equity seems to be a very simple calculation — the total amount of mortgages owed subtracted from the current market value of a home. Here is a simple example:

Current Home Market Value $325,000

Existing Mortgage $225,000

Homeowner Equity $100,000

One side of the equation is well defined, and it is found on the monthly mortgage statement, the loan balance. The other side is less obvious — the current market value of the property.

As a homeowner, your down payment purchases your initial equity, and your monthly (or additional) principal payments increase your equity. In strong real estate markets and in-demand locations, equity can increase quite rapidly as the property value increases, but the inverse can also happen — too much available inventory and market down-cycles can lead to falling home values and a reduction in homeowner equity.

It can be difficult to put an accurate value on something that you have emotional and monetary vesting in. It is safe to say that most people think their home is worth more than then it is.

Homeowners can make savvy assessments about their home’s current market value by following the sales of similar properties in the neighborhood, but should stay away from websites such as Zillow and Trulia, which provide inaccurate and outdated estimates. The most accurate measurement requires a comparative market analysis from a real estate professional or having the home professionally appraised. But, the bottom line — your home is worth as much as someone is willing to pay for it.

Creating Value is in Your Hands

Maintaining the condition of a home is vitally important to retaining and increasing value. Homes are judged against their peers: how they compare to similar homes in the neighborhood. Another way to retain value is to not over upgrade, since it is rare to ever recoup the money spent if you exceed neighborhood value. Keep up the landscaping and do the little things to add curb appeal.

Putting Home Equity to Work

Home equity represents the largest single asset of millions of people, and because it represents so much of an individual’s net worth, it must be treated with respect. Home equity is not a liquid asset until a property is sold, or it is borrowed against.

There are two types of loans that tap into homeowner equity as collateral.

Home Equity Loans

Many home equity plans set a fixed period during which the person can borrow money, such as 10 years. At the end of this “draw period,” the person may be allowed to renew the credit line. If the plan does not allow renewals, the homeowner will not be able to borrow additional money once the period has ended. Some plans may call for payment in full of any outstanding balance at the end of the period. Others may allow repayment over a fixed period, for example, of 10 years.

A home equity loan, sometimes called a second mortgage, usually has a fixed rate and a set time to pay it back, generally with equal monthly payments.

Home Equity Line of Credit

A home equity line of credit is similar to a credit card. The lender sets a maximum amount you can borrow, and you can draw money as you need it, though many home equity lines of credit require an initial draw. The interest rate varies daily, and is usually prime plus a set number, but the required payment is usually interest only. Once the loan has been paid down, the payment is reduced, and it can be paid off and initiated as many times as a homeowner requires.

How Much Equity can be Accessed?

Since the financial institution is lending money and using a home as collateral, they will not lend 100% of the home’s equity. The bank does not want to take the risk that if the house price drops, they would be carrying a loan for more than its market value. Therefore, most banks will allow a qualified homeowner to borrow approximately 80% of their equity.

It’s Important to Use Your Home Equity Wisely

Because it is likely the biggest asset most people have, losing your home equity is hard to overcome. It must be used in prudent ways, and the payments against the loan must be affordable. Using equity money to make the loan payment is only acceptable for a short-term solution.

There are number of good reasons to use money from a home equity loan… and some really bad ones. First, let’s cover smart uses.

1. Invest in Your Home

The best way to use the money is create more equity in the home. Among the very best returns on your investment (ROI) include kitchen and bathroom remodels, adding square footage or an extra bath, enhancing curb appeal and repairing/keeping the existing structure sound. Making prudent investments in your home is a wonderful win-win: you enjoy the upgrades and the repairs can add value to the home.

2. Invest in your Children’s Education

Using your home equity to finance a child’s higher education may be the greatest payoff of all. Not only is the rate much lower than a student loan, it is an investment in the child’s future.

3. Supplement Retirement Needs

Older homeowners spent their working lives paying down their mortgage. At retirement, when monthly income is reduced, a home equity loan could pay for a dream vacation or an unexpected major expense.

4. Augment the Impending Sale of a Home

If you’re planning to sell soon, a home equity line of credit may be the best way to finance improvements, and you can pay it off entirely when you sell. Investing wisely on upgrades and repairs may even reap a profit on your investment.

Here are some examples of some not very wise choices.

Adding luxury amenities like a swimming pool, a hot spa, lavish landscaping, expensive appliances and exotic countertops and flooring rarely pay off.

Purchasing a car or boat or most any personal luxury items is a poor use of the funds, since these items quickly depreciate in value.

Also stay away from using money on risk-heavy investments. Financing stock purchases, start-up businesses and paying routine bills is not financially smart. If you cannot afford to purchase those items with available funds, using equity from your home means they should not be in your budget.

You should treat a home equity loan as an investment and not as extra cash when making financial decisions. If your intended use of the money doesn’t pay you back in some way, it’s not the best use of your valuable equity.

We Are Happy to Assist You

If you would like an assessment of the market value of your home and the current equity you can access, give us a call at 303-475-6269 or email 2johnfarley@gmail.com for a comparative market analysis.

by Farley Webmaster | Aug 29, 2016

Okay, you made one of the most important decisions in your life: you’re buying a home! You found your ideal home. It’s in your desired neighborhood, close to everything you love, you dig its design and feel, and you’re ready to finalize the deal.

But, whoa … wait a minute! Buying a home isn’t like buying a toaster. If you discover something’s wrong with your new home, you can’t return it for a refund or an even exchange. You’re stuck with your buying decision. Purchasing a home is an important investment and should be treated as such. Therefore, before finalizing anything, your “ideal” home needs an inspection to protect you from throwing your hard-earned money into a money pit.

A home inspection is a professional visual examination of the home’s roof, plumbing, heating and cooling system, electrical systems, and foundation.

There are really two types of home of inspections. There is a general home inspection and a specialized inspection. Most general inspections cost between $267 and $370. The cost of the specialized inspection varies from type to type. If the inspector recommends a specialized inspection, take that advice because buying a home is the single most important investment you’ll make and you want extra assurance that you’re making a wise investment.

By having your prospective new home inspected, you can:

- Negotiate with the home seller and get the home sale-ready at no cost to you

- Prevent your insurance rates from rising

- Opt-out of the purchase before you make a costly mistake

- Save money in the short and long run

How Much Money Can a Home Inspection Save You?

A home inspection helps to find potential expenses beyond the sales price, which puts homebuyers in a powerful position for negotiation. If there are any issues discovered during the home inspection, buyers can stipulate that the sellers either repair them before closing or help cover the costs in some other way. If the sellers do not want to front the money to complete the repairs, buyers could negotiate a drop in the overall sales price of the home!

Perhaps even more importantly, a home inspection buys you peace of mind. Your first days and months in a new home will set the tone for your life there, and you don’t want to taint that time with worries about hidden problems and potential money pits.

To help you understand how much money a home inspection can save you, here are some numbers from HomeAdvisor to drive the point home … so to speak.

Roof – Roofing problems are one of the most common issues found by home inspections. Roof repair can range between $316 and $1046, but to replace a roof entirely can cost between $4,660 and $8,950.

Plumbing – Don’t underestimate the plumbing. Small leaks can cause damage that costs between $1,041 and $3,488 to repair. Your home inspector will look for visible problems with the plumbing such as leaky faucets, water stains around sinks and the shower, and noisy pipes. Stains on walls, ceilings, and warped floors show plumbing problems.

Heating and Cooling – Ensuring the home’s heating and cooling system is working properly is very important. Your home inspector will make you aware of any problems with the existing system and let know you whether the system is past its prime and needs replacing. You don’t want to throw down $3,919 to replace an aged furnace. Nor do you want to spend $5,238 replacing an ill-working air conditioner. Replacing and repairing a water heater gets pricey too. Wouldn’t you rather use your savings for a vacation?

Electrical Systems – When thinking of the electrical system, no problem is better than even a small problem. Electrical problems might seem small, but they can blossom into thousand-dollar catastrophes. Make sure your home inspector examines the electric meter, wires, circuit breaker, switches, and the GCFI outlets and electrical outlets.

Foundation – If your home inspector sees that the house is sinking, that means water is seeping into the foundation; cracks in walls, sticking windows, and sagging floor also indicate foundational problems. The foundation is so important that if the general inspection report shows foundation problems, lenders will not lend money on the home until those issues are solved. Foundation repairs can reach as high as $5,880 to repair.

As you can see, a small investment of a few hundred dollars for a general home inspection can save you tons of money and future headaches. To save even more money, you might consider investing in a specialized home inspection as well. A specialized inspection gets down to the nitty-gritty of all the trouble spots the general home inspection might have located.

How Much Money Can a Specialized Inspection Save You?

A general home inspection can trigger a need for a specialized inspection because the general home inspector spotted something off about the roof, sewer system, the heating and cooling system, and the foundation. If humidity is high where you’re buying your home, a pest inspection is recommended. Usually, a pest inspection will check for mold as well as pests. Most homebuyers have a Radon test done to ensure air quality.

Roof – Roof specialists examine the chimney and the flashing surrounding it. They also look at the level of wear and tear of the roof. They can tell you how long the roof will last before a new one is needed. They’ll inspect the downspouts and gutters. The average cost of a roof inspection is about $223. Most roof inspections will cost between $121 and $324.

Sewer System – Making sure your sewer system has no problems should happen before the closing because what might look like a small problem can turn into a large problem in the future. If any issues pop up, you can negotiate with the seller about needed repairs or replacements before closing. Cost of inspection will vary; on the low side, it might cost you around $95, and on the high side, it might cost you $790. Compare these numbers to repairing a septic tank, which can cost, on average, $1,435 (though it could reach as high as $4,459), and you can see that the cost of an inspection is worth it when you catch the problem before you buy.

Heating and Cooling System – A HVAC specialist will check the ducts for blockage and for consistent maintenance of the unit. The repairs needed might be small or they might be big, but this small investment will save you headaches and lots of money down the road.

Foundation – A foundation specialist will pinpoint the exact problem with the foundation. The specialist will look at the grade or slope of the home. The ground should slope away from the home in all directions a half inch per foot. Most homeowners have spent between $1,763 and $5,880 to repair their foundation. And the average cost to re-slope a lawn is at $1,705. Most homeowners paid between $933 and $2,558 to re-slope their lawn.

Pest Inspection – Termites eat a home’s wood structure from inside out and can cause thousands of dollars worth of damage to your home. Other pests can turn your dream home into a nightmare. Depending on the humidity of where you live, you should a pest/termite inspection every two years or so. You can start with your potential new home. Most inspections are extensive and cost between $109 and $281. The good news is that most pest management company will guarantee the past inspection if bugs show up.

Radon Test – Radon is a naturally occurring invisible odorless gas that is the second leading cause of cancer. A radon test is a good test to have done as a good habit. The cost of radon test is low and its cost varies from state to state. Here’smore information about Radon.

Steps You Can Take to Save Money Using a Home Inspection

To help yourself save with a home inspection, you will need to:

Attend the inspection – Attending the inspection is important because it’s an opportunity for you to ask questions.

Check utilities – Checking utilities let’s know the energy efficiency of your potential home.

Hire a Qualified Home Inspector – We can recommend bona-fide home inspectors to you. You can compare our recommendation with all inspectors who belong to the American Society of Home Inspectors. While the decision of who you work with is always yours, we can educate you so that you make a wise homebuying decision.